You've just arrived in Canada, passport stamped and plans packed. The first week is a sprint: SIN number, Canadian cell phone, a permanent address—our first 30 days checklist covers it all. Somewhere in that rush, one task often gets pushed back: opening a Canadian bank account. That delay can cost you more than you expect.

Without a Canadian bank account, you cannot receive your salary by direct deposit, rent a decent apartment, start building a credit history, or move money without paying steep fees on every transaction. The sooner you open an account, the sooner those costs stop.

This guide was put together by the team at UP Immigration Consulting (RCIC Larissa Castelluber, R710678) in Vancouver, BC, based on what newcomer clients report every week about the Canadian banking process in 2026. We cover the Big Five banks, newcomer programs, required documents, how to get a credit card without a credit history, and the mistakes that drain money.

Why open an account in your first month

There are three practical reasons this is urgent, not optional.

Receiving your salary. Canadian employers almost always pay by direct deposit. They ask for a void cheque or a pre-authorized debit form with your account details. Without a Canadian account, you delay your first payment and signal to HR that you are not yet settled.

Renting an apartment. Landlords ask for first and last month's rent transferred by Interac e-Transfer (Canada's equivalent of an instant bank transfer) or a certified cheque. Many also require pre-authorized debit to collect monthly rent. Paying with an international transfer is expensive, slow, and raises questions about whether you have local income.

Avoiding unnecessary fees. Every transaction you make with a foreign card while living in Canada costs you a currency conversion fee plus your home bank's spread. Over three months, those charges can add up to a significant amount. A Canadian account eliminates that drain immediately.

The Big Five Canadian banks

Canada's banking sector is dominated by five institutions known as the Big Five. All of them have branches in almost every mid-sized city, solid mobile apps, and some form of newcomer program.

RBC (Royal Bank of Canada), the country's largest bank, offers a robust Newcomer Advantage program and has a wide presence across British Columbia and Ontario.

TD (Toronto-Dominion), strong in Ontario and the East Coast, with extended branch hours (many locations open Saturdays) and a well-structured New to Canada program.

Scotiabank, historically the most internationally oriented of the five, with a long track record of serving newcomers from many regions. Their StartRight program is a reference point for immigrants.

BMO (Bank of Montreal), NewStart program with solid benefits, known for being responsive in Quebec and Ontario.

CIBC, Newcomer to Canada program, with a strong partnership with Air Canada Aeroplan for frequent travellers.

There is no universally "best" bank. The right choice is the one with a branch near your home or workplace, staff who can assist you effectively, and a newcomer program that fits your situation.

Newcomer program comparison

The table below compares the main benefits offered to permanent residents, temporary foreign workers, and international students within their first five years in Canada. Conditions and fees change, so confirm the details at a branch or on the bank's website before deciding.

| Bank | Free banking period | SIN required to open | Credit card without history | International cheque exchange |

|---|---|---|---|---|

| RBC | Up to 12 months (No Monthly Fee Bank Account) | Not required at opening | Yes, initial limit CAD 500–2,000 | Yes, USD and other currencies |

| TD | Up to 12 months (Unlimited Chequing) | Not required at opening | Yes, via New to Canada program | Yes, case-by-case policy |

| Scotiabank | Up to 12 months (StartRight) | Not required at opening | Yes, Scotiabank Passport Visa Infinite accessible | Yes, strong international focus |

| BMO | Up to 12 months (NewStart Performance) | Not required at opening | Yes, BMO CashBack Mastercard without history | Yes |

| CIBC | Up to 12 months (Smart Account) | Not required at opening | Yes, Newcomer program | Yes, Aeroplan partnership |

Note: "free banking" means the monthly account fee (typically CAD 16.95) is waived during the promotional period. Other fees such as overdraft, NSF, and international transfers still apply.

Required documents

The standard document list at any of the Big Five:

- Valid passport (original, not a copy)

- Proof of immigration status: PR card, COPR (Confirmation of Permanent Residence), work permit, or study permit

- Proof of Canadian address: rental agreement, utility bill (Hydro, internet), or a letter from your employer showing your address

You do not need your SIN (Social Insurance Number) to open an account. You can open the account first and provide the SIN later. Some account features, such as interest-bearing accounts that need to be reported for tax purposes, require a SIN on file, but a basic chequing account works without it.

For a complete overview of your first 30 days in Canada, including SIN setup, see our newcomer arrival checklist.

Chequing vs. Savings account

These are two account types you will hear about immediately. Understanding the difference before signing anything saves confusion later.

Chequing account, your everyday account. Receives salary deposits, pays rent, issues cheques. Earns little to no interest. This is the account you need on day one.

Savings account, earns interest (in 2026, ranging from approximately 1.5% to 4% per year depending on the bank and account type). There is no debit card attached, and most savings accounts charge a fee if you make more than one or two outbound transfers per month. It is designed for your emergency reserve, not daily spending.

A common approach among newcomers is to open both a chequing account and a savings account at the same bank on the first visit.

How to get a credit card without a Canadian credit history

This is the part that catches most newcomers off guard. In many countries, a bank will issue a credit card based on your income. In Canada, lenders look at your credit score, which you do not have yet when you arrive.

Two approaches work:

Newcomer credit card through a bank program. All Big Five banks offer this as part of their newcomer package. You do not need a Canadian credit score, but you must be within the eligible window, generally within five years of arriving as a permanent resident or temporary resident. Initial limits are typically CAD 500 to 2,000.

Secured credit card. You deposit a security deposit, normally CAD 200 to 1,000, and your credit limit equals that deposit exactly. You use the card like a regular credit card, pay the bill each month, and the bank reports your payment history to Equifax and TransUnion. Your score begins to grow. After 12 to 18 months of responsible use, you can apply for an unsecured card and get the deposit back. The Home Trust Secured Visa is the most widely used option.

The core rule: keep your balance at 30% or less of your limit, and pay the full statement balance every month, not just the minimum. This builds your score quickly.

How to build your credit score from zero

Your Canadian credit score starts with no history and runs from 300 to 900. Most landlords and lenders want to see 650 or higher before approving you without a co-signer or extra conditions.

Four actions build your score efficiently:

- Use a credit card (newcomer or secured) responsibly every month

- Put bills in your name (cell phone, internet), as some providers report payment history to the credit bureaus

- Keep older accounts open, since length of credit history is a factor in your score

- Avoid applying for too much credit at once, each hard inquiry temporarily lowers your score

A realistic timeline: six months to establish a score, twelve months to reach a good score, twenty-four months to have a score that opens the door to a mortgage.

Sending money internationally

Moving money from abroad to Canada is one of the areas where newcomers most commonly overpay. A traditional wire transfer from an overseas bank typically carries a transfer fee of 1% to 3%, plus a currency conversion spread that can be significant depending on the provider.

Wise (formerly TransferWise), uses the mid-market exchange rate plus a transparent fee. In 2026, the all-in cost typically runs between 0.5% and 1%. The money arrives in CAD directly in your Canadian bank account within one to three business days.

Remitly, competitive for smaller amounts (up to approximately CAD 1,500 to 2,000), with an "Economy" option that costs less if you can wait three to five business days for delivery.

Western Union, available at physical locations. Convenient in an urgent situation, but the exchange rate spread is considerably worse than Wise. Use only when speed at a branch is the priority.

Wire transfer via a traditional bank, the most expensive option in most scenarios. Consider it only when you need to move a large amount (above CAD 10,000) and require formal traceability for tax or compliance purposes.

Common mistakes that cost money

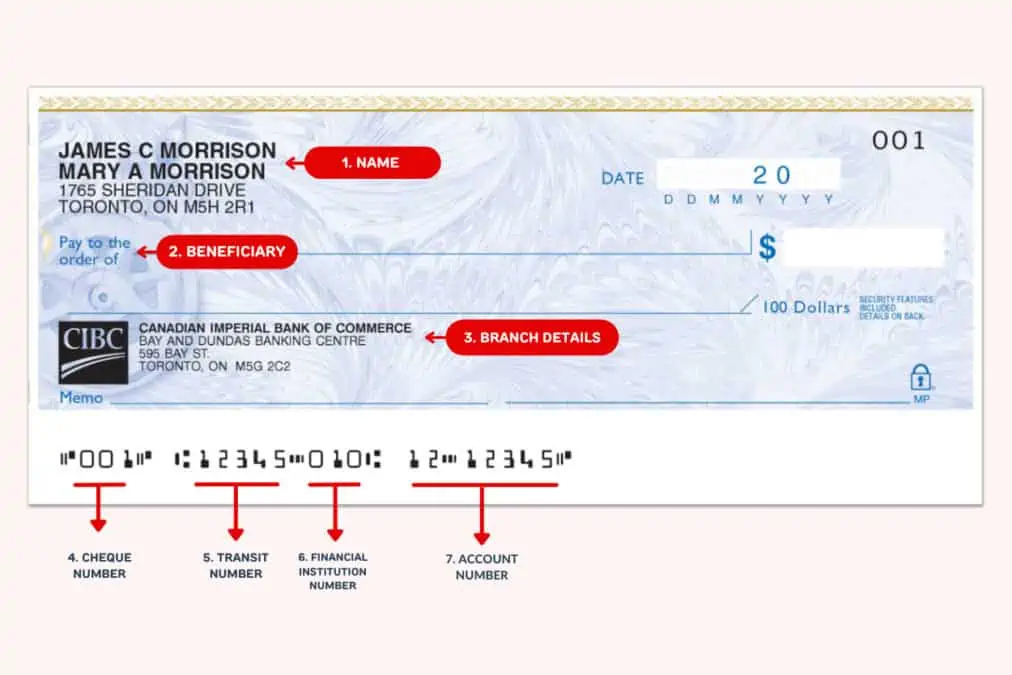

Not activating Interac e-Transfer. This is Canada's instant bank transfer system, similar to peer-to-peer payment apps in other countries. You send money by email or phone number, it arrives in seconds, and most newcomer accounts include it at no extra charge. Without it active, you end up relying on cheques to pay rent or split costs. Ask the bank teller to activate it when you open the account, set your security question, and test it by sending a small amount to yourself.

Not requesting a cheque book at opening. Some landlords still require a void cheque to set up pre-authorized debit. Without one, the process stalls. Ask for a cheque book when you open the account (it costs approximately CAD 30 to 50), or at minimum print a void cheque from your bank's mobile app.

Missing the fee structure after the newcomer promotion ends. Once the free banking period concludes, the monthly fee resumes. In most cases, you can waive it by maintaining a minimum balance (CAD 3,000 to 5,000 depending on the bank) or by switching to a lower-tier account. Mark your calendar eleven months after opening to review your options before the fee kicks in.

Conclusion and next step

Opening a Canadian bank account is one of the first practical milestones that helps you feel settled. Done right in the first week, it unlocks direct deposit, rental applications, credit history, and lower transfer costs. Done late, it means paying unnecessary fees and missing out on housing and employment opportunities.

If you are still planning your move and deciding between Express Entry, a work permit, a study permit, or another pathway, the immigration strategy you choose affects what newcomer programs you qualify for and when you can open an account. Getting that right from the start matters.

Schedule a consultation with RCIC Larissa Castelluber to review your immigration pathway before you arrive. Her team works with PR applicants, temporary residents, and students navigating life in Canada.